State of the Market – European Review Q1 2023

Activism and Shareholder Engagement

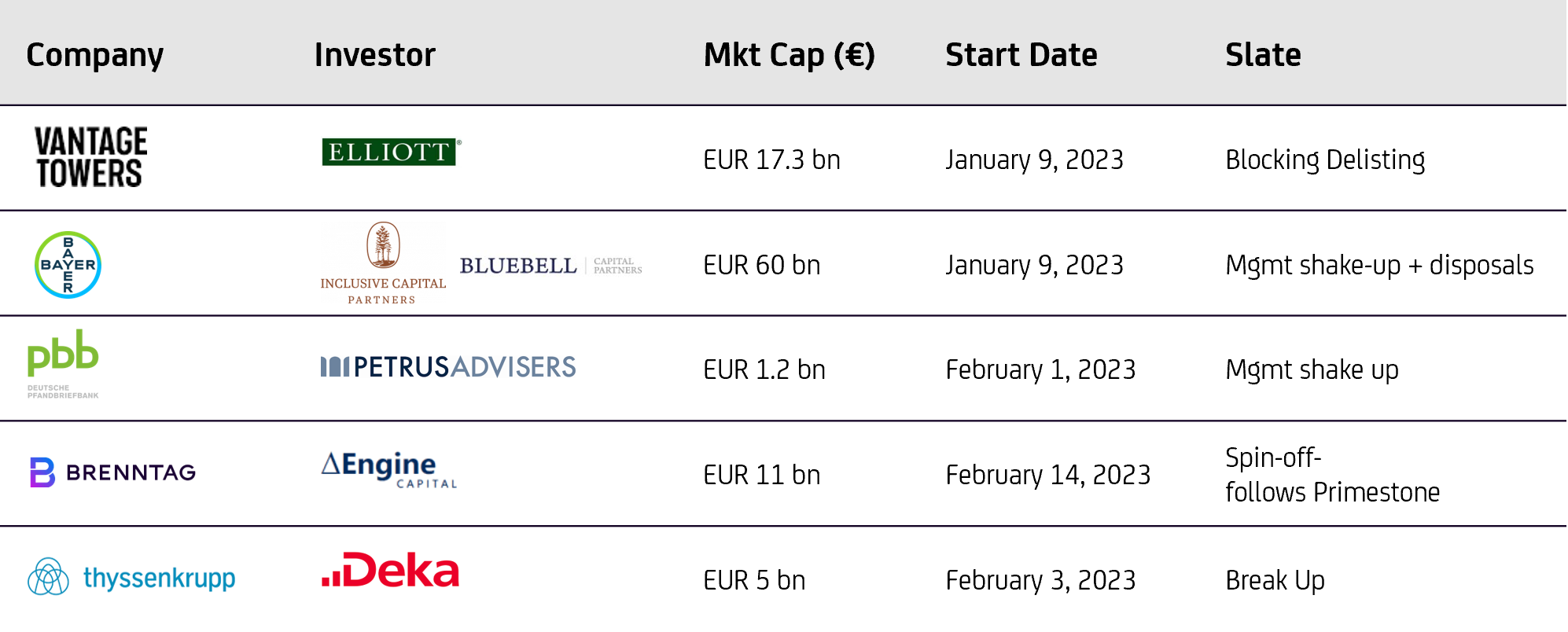

#5

Campaigns 2023

The most targeted sectors have been Consumers and Industrials

19%

15%

12%

8%

Consumer Discretionary

Industrials

Materials

Financials

Health Care

Communications

Others

... while Germany saw record start of the year in activism campaigns:

50%

United Kingdom

23%

Germany

4%

France

Norway

Belgium

Netherlands

As of March 2023, the number of New Activism Campaigns in Europe is #26 ytd

Summary

2023 started with a sharp increase in number of activism campaigns driven by break-up requests.

Germany saw record start of the year with #6 new campaigns as low valuations coupled with country-specifics are attracting activist investors.

New actors are entering the activism arena and acting in concert pushing for different changes particularly in large-companies as they see them as "defensive" play in this volatile environment – experts call this trend "wolfpack" attack.

Number of campaigns soars in the first quarter of 2023, as activists set for a new wave of attacks on companies

Q3

Q4

Q2

Q1

24

43

74

82

101

98

110

87

2015

2016

2017

2018

2019

2020

2021

2022

2023

26

6

11

20

13

25

29

32

22

+18%

Learn more

2023 started with large companies being the target of activism because they are viewed as a "defensive" play to put money in a volatile economic environment.

What are activists asking in 2023?

Break-up and board representation are the most popular requests – activists see break-up as the quickest way to unlock value and they want to be the ones to lead this change!

Board Representation

Buyback

Oppose Acquisition

Cost Cutting

Break Up

31%

21%

10%

7%

2023 ACTIVISTS REQUESTS BREAKDOWN (%)

Blocking a deal slate, that soared in 2022, continued both globally and in Europe in the first quarter of 2023.

Case Study

Wolfpack Strategy

More and more actors are entering in the activism arena: Large companies are particularly vulnerable to these packs of agitators that may not even have the same agenda but they act in coordination to make their prey weaker and weaker.

< USD 500 m

27%

USD 500 m – USD 1 bn

USD 1 bn – USD 5 bn

USD 5 bn – USD 10 bn

> USD 10 bn

38%

% 2023 EU Campaigns by Market Cap

Client Solutions is a division of UniCredit Group and consists of UniCredit Bank AG, Munich, UniCredit Bank AG Vienna Branch, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit S.p.A., Rome and other members of UniCredit. UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank. In addition, UniCredit Bank AG is regulated by the Federal Financial Supervisory Authority (BaFin). In addition to that, UniCredit Bank AG Vienna Branch is also regulated by the Austrian Financial Market Authority (FMA), UniCredit Bank AG London Branch is also regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) and UniCredit Bank AG Milan Branch is also regulated by Banca d’Italia and the Commissione Nazionale per le Società e la Borsa (CONSOB). UniCredit S.p.A. is regulated by Banca d’Italia and the Commissione Nazionale per le Società e la Borsa (CONSOB). This publication is intended for marketing purpose only and it is published by UniCredit Group. Under no circumstances may the information contained in the published material be construed as an offer, recommendation, invitation to offer or promotional message for the purchase, sale or subscription of financial products. This marketing communication is directed solely at investment professionals and constitutes a “non-retail communication” for the purposes of the relevant rules.

2023 Q1 Update

CASE Study

A&SE Services

Legal Framework Episode #1

© 2023 UniCredit S.p.A. - All Rights reserved

UniCredit

General Company Info

Privacy

Disclaimer

Accessibility

Case Study Bayer

ESG and Shareholder Base

Business Operation

Return and Valuation

Vulnerability Index is 58.8 – very high compared with industry and German average, meaning the Company is under activists screening; Total Shareholder Return should be monitored as a deterioration could increase dissatisfaction among shareholders; Valuations are very low and FCF evolution is under scrutiny. The board tenure is too high with a member sitting there for more than 20 years.

Our Vulnerability Index fully intercepted Bayer Case

The Result

The Activists

The Request

The Case

In 2018 Bayer finalised the acquisition of the agribusiness giant Monsanto for USD 63 bio, widely regarded as one of the most damaging acquisitions in recent times as Bayer’s stock was down almost 50% a year after the deal completion, never recovered from there.

The Catalyst

Timing is important. Activists wait for the right catalyst to attack; in the Bayer Case the catalyst was the upcoming end of the employment contract for its chief executive – Werner Baumann – heavily criticized by shareholders since he engineered the Monsanto deal.

Elliott Investment – 2019, >2% stake Bluebell – 2022, stake not disclosed Inclusive Partners – 2023, 0.8% stake

The Activist

In February 2023 Bayer has appointed Roche’s former head of pharmaceuticals Bill Anderson as new CEO. Werner Baumann will leave by the end of May, almost a year before his contract expires. Shares rose 6% after the announcement. The new CEO states that his ambition is to "accelerate innovation, increase performance, advance sustainability and unleash the full potential of the company”.

Results as of today

Replacement of CEO Refreshment of the Board Break Up

58.8

Vulnerability Index

The full range of our offer

More than 30 activities provided by UniCredit Team to secure and protect the Company from activist potential attacks and proactively engage with shareholders ...

Vulnerability Assessment

Shareholder Support Analysis

Stakeholder Engagement

Explore Penetration Angles

Activists Monitoring & Watch List

ESG Attack Points Analysis

Shareholder Structure Analysis

Shifts in Ownership

Vote Projections

Communication Strategy

“Ready” Team & Response Protocol

Proactive Engagement

Defense Playbook

Centralised Monitor Platform

Campaign Management / Coordination

Shareholder Info Collection

Market Sentiment Dashboard

Shareholder Base Intelligence

Independent Review

Ready Team

Strategic White Paper

Statement of Defense

Campaign Maneuvers

Activists Matrix

For Investor Relations

For Management and Board

By failing to prepare, you are preparing to fail

Michele Troiani

Managing Director Head of Activism & Shareholder Engagement Advisory & Capital Markets

Michele.Troiani@unicredit.eu

Luca Azzara

Associate Director, CFA Activism & Shareholder Engagement Advisory & Capital Markets

Luca.Azzara@unicredit.eu

Contacts

German Domination Agreement

Domination Agreement

Activists, with Elliott being the pioneer of this approach, have frequently muscled in on such situations accumulating shares to prevent the acquirer’s ability to conclude the domination agreement after the takeover, or – failing this – challenging the compensation and pay-out terms offered in the agreement.

The agreement is usually forever, but renegotiable after 5 years.

a. The domination agreement must include an offer to acquire the shares of the target company b. The dominating shareholder must pay a guaranteed dividend to the remaining minority shareholders c. The dominating shareholder must compensate the target company for any annual loss it suffers

In an M&A deal, the bidder needs 50% of a company’s shares to force changes to its supervisory board and influence strategy but to control the target’s cash flows, he must secure 75% of votes in the shareholder meeting in support of the so-called “domination agreement”. The remaining minority shareholders then surrender their voting rights to give the acquirer outright control. In return, the newly gagged minorities get the option to sell their shares for a “fair” amount to be determined by independent assessors and the courts. Until that day comes, they collect an annual payment that is supposed to replace the dividends they aren’t getting in the meantime.

The domination agreement is a unique procedure under the German Law that makes completing a deal tougher, as it is a necessary condition for an acquirer to avail itself of the target’s assets to pay for the acquisition price.

Why do activists love it?

How long does it last?

What should be included?

How does it work?

What is it?